What Is Income Verification?

Income verification is the process of confirming an applicant's earnings from a third-party source to validate their stated income. Mortgage lenders, tenant screeners, and consumer reporting agencies use income verification to assess creditworthiness, determine loan qualifying amounts, and evaluate rent-to-income ratios.

Income verification differs fundamentally from employment verification. Employment verification confirms job status, dates of employment, and position title. Income verification goes deeper — it confirms salary amounts, pay frequency, bonuses, overtime, and total compensation history.

The distinction matters because requestors often need both pieces of information. A mortgage lender might verify employment status to confirm job stability while simultaneously verifying income to calculate debt-to-income ratios. A tenant screener might confirm current employment but focus primarily on monthly earnings to assess rent affordability.

The income verification process requires contacting employers, payroll providers, or reviewing financial documents to obtain compensation data. This third-party confirmation prevents applicants from inflating their earnings and gives requestors confidence in their underwriting decisions.

Income Verification vs. Employment Verification: What's the Difference?

Employment verification confirms whether someone works at a company and their job title, start date, and employment status. Income verification goes deeper — it confirms actual earnings, pay frequency, salary amounts, and compensation history.

Mortgage lenders typically need both pieces of information. They verify employment to ensure the borrower has a stable job, then verify income to calculate debt-to-income ratios and qualifying income under lending guidelines.

Tenant screeners often focus primarily on income verification since landlords care more about rent-to-income ratios than employment dates. A tenant earning $5,000 monthly from freelance work matters more than their job title at a traditional employer.

Some scenarios require only employment verification. Background check companies verifying past work history for hiring decisions don't need salary details. Conversely, disability benefit determinations may require income verification without current employment status.

The verification methods differ too. Employment verification often relies on HR departments confirming basic job details. Income verification requires access to payroll systems, tax records, or detailed pay documentation — information that's harder to obtain and more closely guarded by employers.

Who Requests Income Verification -- and Why

Three types of organizations routinely request income verification, each with distinct business reasons. Mortgage lenders need verified income to calculate debt-to-income ratios and determine loan eligibility under underwriting guidelines. Tenant screeners use income data to evaluate rent-to-income ratios and assess rental application risk.

Consumer reporting agencies (CRAs) perform income verification on behalf of their clients — banks, property management companies, and other businesses that lack direct verification capabilities. CRAs aggregate verification requests and provide results back to the requesting party.

All three requestor types must comply with Fair Credit Reporting Act (FCRA) permissible purpose requirements. Income verification counts as consumer reporting activity, meaning requestors need legitimate business reasons and proper consumer authorization before initiating verification requests.

The verification urgency varies by requestor. Mortgage lenders face closing deadlines and regulatory timelines. Tenant screeners compete for qualified renters in tight rental markets. CRAs balance client expectations with verification complexity, particularly when dealing with hard-to-reach employers that don't participate in automated systems.

Understanding who requests income verification helps explain why multiple verification methods exist — different requestors face different constraints, timelines, and employer coverage needs.

The Three Methods of Income Verification

Income verification follows a decision tree, not a hierarchy. The right method depends on the applicant's employer type and available data sources. No single approach works for every scenario, which is why effective income verification requires a multi-method strategy.

Large employers with integrated payroll systems favor database lookups. Small businesses without digital infrastructure require direct outreach. Self-employed applicants need document-based verification. Understanding when each method applies prevents delays and improves completion rates.

Payroll Database Lookup

Database verification delivers instant results through API connections to major payroll providers like ADP, Paychex, and Workday. The requestor submits the applicant's Social Security number and employer name, receiving current salary, pay frequency, and recent earnings history within seconds.

Coverage limitations create significant gaps. Payroll databases capture roughly 60% of the U.S. workforce, missing small businesses that handle payroll internally, nonprofit organizations, government agencies, and gig economy workers. Fortune 500 companies participate reliably; local restaurants, construction firms, and professional services typically do not.

Database verification fails when employers use manual payroll systems or choose not to share data with third-party platforms. The method also struggles with recent job changes, as database updates can lag by several pay periods. When databases return "no match" results, requestors must pivot to alternative verification methods rather than assuming the applicant provided false information.

Document Review (Pay Stubs, Tax Returns, Bank Statements)

Document review requires applicants to submit financial paperwork directly to the requestor. Pay stubs show recent earnings, tax returns reveal annual income history, and bank statements display deposit patterns. This method captures self-employed contractors, gig workers, and employees at small businesses that payroll databases routinely miss.

The fraud risk runs high with applicant-submitted documents. Pay stubs can be fabricated using online generators, tax returns can be altered, and bank statements can be doctored. Manual review becomes necessary to spot inconsistencies, watermark tampering, and formatting irregularities that signal falsification.

Processing document-based income verification creates operational bottlenecks. Underwriters must manually calculate annualized income from irregular pay periods, cross-reference multiple document types for consistency, and request additional paperwork when initial submissions prove incomplete. Small mortgage shops and tenant screeners often lack dedicated staff to handle this review workload efficiently.

Document review works best for borrowers with complex income structures that databases cannot parse. Real estate agents earning commission, freelance consultants with multiple clients, and seasonal workers with variable pay schedules all require human analysis of their earning patterns. The manual burden justifies the cost only when automated methods cannot reach the employer or when applicant income defies standard W-2 categorization.

Employer Outreach (Phone, Email, Fax)

Direct employer contact serves as the universal fallback when payroll databases hit coverage gaps and document review proves insufficient. This method reaches every employer — from small businesses with self-managed payroll to nonprofits operating outside commercial databases.

The process involves contacting HR departments or payroll administrators through multiple channels simultaneously. Phone calls navigate automated systems and reach decision-makers. Email requests provide documentation trails. Fax submissions satisfy employers preferring traditional communication methods.

Employer outreach excels where automation fails. Small employers rarely participate in commercial databases. Self-employed applicants may lack traditional pay stubs. Seasonal workers present inconsistent documentation patterns.

The challenge lies in operational scale. Manual outreach requires significant time investment per verification request. Phone trees delay contact attempts. Voicemail chains extend turnaround times. Email responses depend on employer responsiveness.

Traditional outreach methods also struggle with compliance documentation. Mortgage lenders must satisfy Fannie Mae's verbal verification requirements within specific timeframes. Tenant screeners need complete audit trails for dispute resolution.

AI-powered outreach systems now automate these employer contacts while maintaining human oversight. Automated agents handle phone navigation, email follow-ups, and fax transmission. Every interaction generates logged records for compliance purposes. This approach delivers database-level speed with universal employer coverage.

When Automated Methods Fail: The Hard-to-Reach Employer Problem

Payroll databases excel at large corporations with enrolled HR systems, but they miss the millions of small businesses, nonprofits, and companies managing payroll in-house. These employers represent a significant coverage gap that leaves requestors scrambling for alternatives when automated lookups return no data.

Document review becomes the default fallback, requiring applicants to submit pay stubs, tax returns, or bank statements. This manual process introduces fraud risk through doctored documents and creates review bottlenecks that slow approval timelines. Self-employed applicants and gig workers often lack traditional pay stubs, forcing lengthy document collection cycles.

Employer outreach emerges as the only method that can reach every employer, regardless of size or payroll system. Direct contact with HR departments or payroll administrators provides authoritative income data when databases fail and documents raise red flags. The challenge lies in scaling manual outreach across thousands of verification requests.

Traditional employer outreach relies on human agents making phone calls, sending emails, and dispatching faxes. This approach works but creates operational constraints: agents handle limited case volumes, phone trees consume time, and follow-up cycles stretch verification timelines. Manual outreach becomes the bottleneck precisely when requestors need it most.

AI-powered employer outreach automates this final verification method, simultaneously contacting employers across multiple channels while maintaining the human touch required for successful income verification conversations.

Compliance Requirements by Use Case

Income verification operates under distinct regulatory frameworks depending on your use case. Mortgage lenders face the strictest requirements, tenant screeners navigate state-specific salary laws, and all requestors must satisfy federal consumer protection standards.

Mortgage Lending: Fannie Mae's 10-Day Rule

Mortgage lenders must complete verbal verification of employment (VOE) within 10 business days of closing. This Fannie Mae requirement ensures employment status hasn't changed between application and funding. Verbal confirmation must include current employment status, position title, and salary — simple payroll database lookups won't satisfy this mandate.

Tenant Screening: Salary History Restrictions

Seventeen states and numerous cities prohibit landlords from asking about salary history during the application process. These salary history bans require screeners to verify current income without referencing past earnings. States like California, New York, and Massachusetts enforce strict penalties for violations.

Universal Requirements: FCRA and Consumer Authorization

All income verification requests require explicit consumer consent and permissible purpose under the Fair Credit Reporting Act. Requestors must document legitimate business need — loan underwriting, tenant qualification, or background screening. Unauthorized income verification violates federal law regardless of the verification method used. Consumer authorization forms must clearly state what information will be verified and how it will be used.

How AI Outreach Automates Employer Contact for Income Verification

AI agents execute employer outreach at scale by contacting HR departments simultaneously across multiple channels — phone, email, and fax. The system navigates phone trees, leaves targeted voicemails when human contact isn't available, and manages callback scheduling without human intervention.

Each AI agent follows scripted workflows that mirror how experienced verification specialists approach hard-to-reach employers. When calling, the agent identifies itself, states the verification purpose, and requests specific income data points required for the loan file. Email outreach includes pre-formatted verification forms attached directly to the initial contact.

The platform logs every interaction — call duration, email delivery status, fax confirmation receipts, and response content — creating a complete audit trail for compliance documentation. This satisfies Fannie Mae's verbal VOE requirements while eliminating the manual workload that bottlenecks traditional verification teams.

AI outreach fills the operational gap when payroll databases lack coverage and document review carries fraud risk. Small businesses, nonprofits, and companies with self-managed payroll rarely participate in database networks, yet they employ millions of mortgage applicants. AI agents reach these employers directly, securing income confirmations that would otherwise require days of manual follow-up from verification staff.

The technology positions itself as the operational layer for complex cases, not as a database replacement. Lenders maintain their existing database relationships while deploying AI outreach specifically for employers that automated lookups cannot reach.

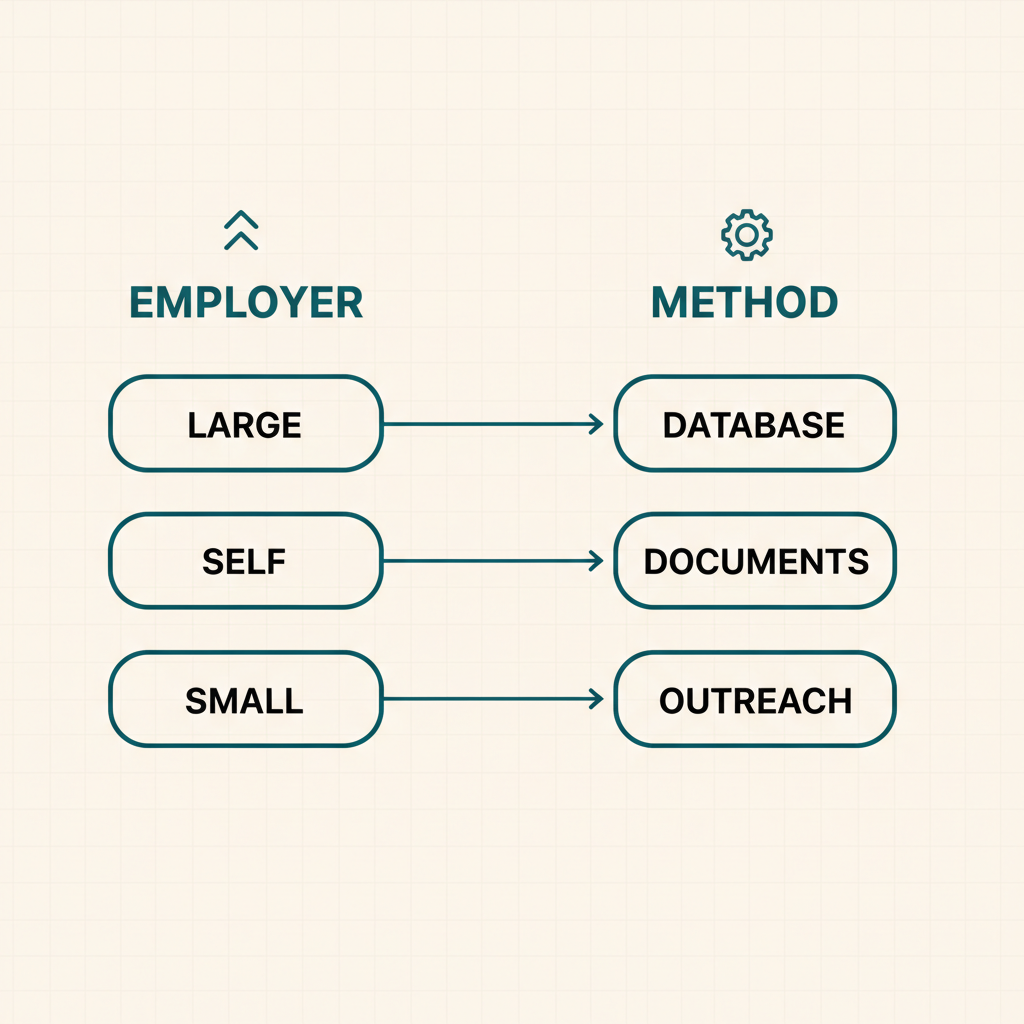

Choosing an Income Verification Method: A Decision Framework

Your verification method depends on three factors: employer size, applicant employment type, and data availability. Large employers with established payroll systems typically participate in verification databases, making automated lookup the fastest option. Self-employed applicants and gig workers require document review since their income doesn't flow through traditional payroll systems.

Small businesses, nonprofits, and companies with internal payroll management rarely appear in verification databases. These employers require direct outreach — phone calls, emails, or fax requests to HR departments. The challenge intensifies when these employers prove unresponsive or difficult to reach through standard channels.

Decision Matrix:

- Large employer (500+ employees): Start with payroll database lookup

- Self-employed/gig worker: Use document review (tax returns, bank statements)

- Small employer/database miss: Deploy employer outreach

- Unresponsive employer: Escalate to AI-powered multi-channel outreach

Most verification workflows combine methods rather than relying on a single approach. Database lookup handles the majority of cases, document review covers self-employed applicants, and outreach fills the remaining gaps. The key is building fallback processes that prevent bottlenecks when your primary method fails.

For detailed provider comparisons across all three methods, see our income verification provider guide.

Frequently Asked Questions

What documents count as income verification? Pay stubs from the last 30-60 days, tax returns (W-2s, 1099s, or full returns for self-employed applicants), and bank statements showing direct deposits. Employer-provided salary letters on company letterhead also qualify, though lenders prefer third-party documentation.

Is income verification required for all mortgages? Yes, for conventional loans backed by Fannie Mae or Freddie Mac. Government loans (FHA, VA, USDA) also require income verification. Cash purchases and some alternative lending products may waive this requirement, but standard mortgage underwriting always includes income confirmation.

Can a landlord ask for income verification? Yes, landlords can request income verification as part of tenant screening, provided they have written consent from the applicant. However, salary history ban laws in states like California and New York restrict what income questions landlords can ask during the application process.

How long does income verification take? Database lookups return results instantly. Document review takes 1-3 business days depending on manual review requirements. Employer outreach typically takes 3-7 business days, though hard-to-reach employers can extend this to 10+ days without AI automation.

What is automated income verification? Automated systems pull income data directly from payroll databases or use AI to contact employers via phone, email, and fax simultaneously, eliminating manual follow-up delays.

Conclusion

Your method selection follows the data trail: payroll databases for enrolled large employers, document review for self-employed applicants, and AI outreach for the small businesses and unresponsive employers that fall through the cracks. Each method serves specific employer types rather than competing for the same use cases.

For complete applicant profiles, pair income verification with employment verification to confirm both job status and earnings. AI outreach becomes your operational backbone when traditional databases hit their coverage limits, ensuring no employer remains unreachable in your verification workflow.