A failed verbal VOE ten days before closing doesn't just delay a loan. It kills deals, triggers buyback exposure, and creates the kind of operational chaos that ripples through a pipeline for weeks. Choosing the right verification provider has become a question of which gaps in your workflow you can actually afford to leave open.

The vendor landscape for mortgage verification has fragmented into four distinct categories, each solving a different problem. Most lenders need more than one. The challenge is understanding which provider fits which scenario, and where compliance risk concentrates.

Why Verification Vendor Selection Matters More Than It Used To

Loan manufacturing timelines have compressed while compliance requirements have stayed rigid. A borrower working for a 12-person landscaping company with no HR department creates the same verbal VOE obligation as a borrower at a Fortune 500 firm. The difference is that one takes seconds to verify and the other can stall a closing for a week.

Buyback risk from insufficient verbal VOE documentation has made this a QC issue, not just an operations inconvenience. When post-closing audits flag a missing or incomplete verbal VOE, the lender absorbs the repurchase cost regardless of whether the borrower is still employed. The vendor you choose for each verification type directly determines how much of that risk you're carrying.

Understanding the Verification Types You're Actually Buying

VOE, VOI, and VOA serve different functions at different stages of mortgage origination, and no single vendor covers all three equally well.

VOE confirms that a borrower currently holds the job claimed on the application. VOI confirms how much the borrower earns. VOA confirms liquid assets and reserves.

The critical distinction most operations teams miss: a database lookup that returns income history is VOI, not VOE. A verbal VOE, which confirms current employment status through direct employer contact, is a separate compliance requirement that database results do not satisfy.

Verbal VOE: The Compliance Step Most Vendors Don't Solve

Fannie Mae's Selling Guide B3-3.1-04 (updated 03/04/2026) requires a verbal VOE for each borrower using employment income to qualify. The verbal verification must be obtained within 10 business days prior to the note date.

Freddie Mac Guide Section 5302.2 requires Form 90 or an equivalent written document in the mortgage file. FHA/HUD Mortgagee Letter 2019-01 requires re-verification of employment within 10 days prior to mortgage disbursement.

The verbal VOE confirms one thing: the borrower is still employed right now. Even if The Work Number returned a full income history last month, the verbal VOE remains a separate, mandatory step that must happen inside the pre-closing compliance window.

Written VOE and Income Verification

Written VOE typically happens earlier in the process, during underwriting. It captures employment details (job title, start date, salary) in a formal document. VOI can come from payroll records, tax transcripts, or bank statement analysis depending on the loan program.

Both written VOE and VOI are well-served by database lookups and payroll aggregators when the employer participates. The verbal VOE at pre-closing is where most verification workflows break down, because it requires someone to actually reach the employer by phone or equivalent contact.

The Four Provider Types and What Each Actually Does

Every mortgage verification provider falls into one of four categories, and the differences between them show up most clearly when the employer is small, unresponsive, or absent from payroll databases.

Payroll Database Solutions (The Work Number, Experian Verify)

Best for: Instant employment and income records on borrowers who work for large, database-participating employers.

Pros:

- Sub-second lookup speed. When the employer is in the database, results come back immediately with no borrower friction.

- Broad large-employer coverage. Major payroll processors feed records into TWN and Experian Verify, covering a significant share of W-2 employees at mid-to-large companies.

- Standardized income history. Returns structured data (pay rate, pay period, employer tenure) that maps cleanly to underwriting requirements.

Cons:

- Small employer gaps. Businesses that don't use participating payroll processors won't appear in any database.

- Does not satisfy verbal VOE. A database record confirms historical income, not current employment status within the 10-day pre-closing window.

Open Banking Solutions (Plaid, AccountChek)

Best for: Verifying income through bank account transaction data and confirming asset reserves.

Pros:

- Direct bank account access. Pulls transaction-level data showing deposit patterns, which can support income verification for non-traditional borrowers.

- Combined VOI and VOA. A single connection can verify both income streams and asset balances, reducing the number of separate verification orders.

Cons:

- Cannot contact employers. Open banking tools verify what's in the borrower's bank account, with no mechanism to reach an employer and confirm current employment.

- No verbal VOE capability. These tools are borrower-facing, not employer-facing, so they cannot fulfill pre-closing verbal VOE requirements.

Payroll Aggregators (Argyle, Truv)

Best for: Pulling structured payroll data directly from the borrower's connected payroll account across a wide range of payroll platforms.

Pros:

- Wide payroll platform coverage. Argyle claims connections covering 90%+ of the U.S. workforce through direct payroll integrations, giving lenders access to granular pay data.

- Structured, machine-readable output. Payroll-sourced data includes pay stubs, W-2s, and employment details in formats that integrate with LOS platforms.

Cons:

- Borrower must connect their account. If the borrower doesn't complete the connection flow, the verification stalls, and conversion rates vary by platform and borrower demographic.

- No direct employer outreach. Payroll aggregators pull data from the borrower's side. They don't call, email, or fax the employer, which means they cannot complete a verbal VOE or reach employers whose payroll system isn't supported.

AI-Agent Outreach (Superunit)

Best for: Completing verbal VOE through direct, automated employer contact, particularly for small businesses and hard-to-reach employers that don't appear in any database.

Superunit operates differently from the other three categories. Rather than pulling data from a database or borrower-connected account, Superunit's AI agents initiate outreach to the employer directly via phone, email, and fax simultaneously. The approach is designed to solve the specific problem of reaching an employer who doesn't have a dedicated HR department, doesn't participate in payroll reporting networks, or simply doesn't respond to a single phone call.

Pros:

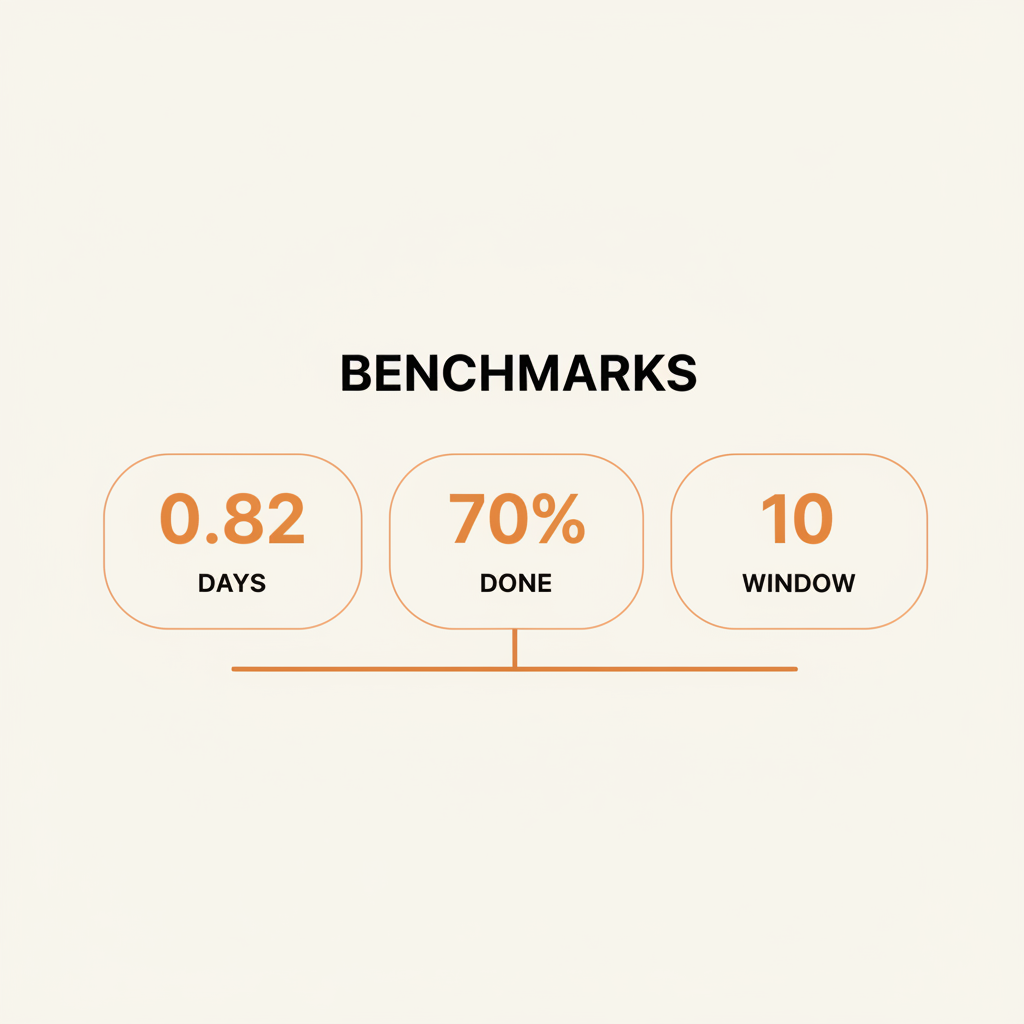

- 0.82 business day average completion. Simultaneous multi-channel outreach produces a sub-one-day average turnaround that fits comfortably inside the 10-business-day compliance window.

- 80% completed within 48 hours. The distribution matters as much as the average. Four out of five verifications close within two business days, giving processors time to escalate the remaining cases.

- Full compliance documentation. Every verification produces call recordings, transcripts, timestamps, and chain-of-custody records. That satisfies Freddie Mac's Form 90 requirements and provides a more complete audit trail than a basic written record, giving QC teams auditable evidence for each verbal VOE.

- Pay-on-success pricing. Lenders pay a flat fee per successful verification. If Superunit can't complete the verification, there's no charge, which removes cost risk on hard-to-reach cases.

- 70% completion rate across verifications. Superunit's volume concentrates on employers other vendors can't reach. A 70% completion rate on that segment is significant, given that these are the cases where manual outreach often produces zero results.

Cons:

- Not a database or income aggregator. Superunit does not return income history, asset data, or payroll records. It confirms employment status through direct employer contact.

- Cannot verify defunct employers. If a business has closed or is unreachable on all channels, no outreach tool can complete the verification.

- Not suited for self-employment. Business owners verifying their own employment need different documentation (tax returns, CPA letters), which falls outside Superunit's scope.

The Decision Criteria That Actually Differentiate Providers

Completion rates on small employers, turnaround time distributions, documentation depth, and effective cost per successful verification separate providers far more than feature lists or coverage claims.

Employer Coverage: Database vs. Direct Outreach

The first question is whether a provider can reach the employer in question. Database solutions work when the employer participates. Payroll aggregators work when the borrower can connect their account. When neither condition is met (common with small businesses, local employers, and startups), direct outreach is the only remaining path.

Ask vendors for their completion rates on employers with fewer than 50 employees. That number will tell you more than any coverage percentage calculated across the entire U.S. workforce.

Turnaround Time Within the Compliance Window

The 10-business-day verbal VOE window is a hard constraint. A provider averaging three to five business days on turnaround consumes half the window on a single verification. A provider that can't complete the verification at all forces the processor into manual phone calls, which may still fail.

Average completion time, measured in business days, is the metric to benchmark across providers. Ask for the distribution, not just the average: what percentage of verifications complete within 24 hours, 48 hours, and 5 business days?

Compliance Documentation Quality

Fannie Mae requires documented evidence of the verbal VOE. Freddie Mac requires Form 90 or equivalent. A handwritten note saying "called employer, confirmed employment" may pass a cursory review, but it won't hold up under a targeted QC audit or repurchase request.

Call recordings, timestamped transcripts, and chain-of-custody records create a defensible audit trail. When evaluating providers, ask to see a sample verification file and compare it against your QC team's documentation standards.

Pricing Model and Cost-Per-Verification

Subscription models charge regardless of outcome. Per-order models charge on submission. Pay-on-success models charge only when the verification completes.

A provider with a low per-order price but a 40% completion rate costs more per successful verification than a provider charging more per order with a higher completion rate. Calculate your effective cost per successful verification, not just the sticker price.

When to Use Each Provider Type: A Practical Framework

| Borrower Scenario | Best Provider Type |

|---|---|

| Large employer, in payroll database | TWN / Experian Verify |

| Income from bank account / assets | Plaid / AccountChek |

| Employer uses supported payroll system | Argyle / Truv |

| Small business, no HR dept, hard to reach | Superunit |

| Tight verbal VOE compliance window | Superunit |

Most production pipelines will route verifications through multiple providers based on employer type. The decision isn't "which one vendor do we pick" but rather "which vendor handles which scenario in our waterfall."

The Hard-to-Reach Employer Problem No Database Solves

Why Small Employers Fall Through Every Database

Small businesses, family-owned companies, and startups rarely participate in payroll reporting networks like The Work Number. They often use basic payroll software (or no software at all), don't have a dedicated HR contact, and may not answer calls from unknown numbers.

A common borrower complaint on Reddit's r/Mortgages captures the frustration: "My loan officer says one of our approval conditions is producing a phone number for HR for employment verification. What are our options?" The borrower often can't solve the problem themselves. The employer may not know what a VOE is, may be suspicious of the call, or may simply not prioritize returning it.

What Happens When the Employer Doesn't Respond

When manual outreach fails, the loan file stalls. Processors spend hours redialing, leaving voicemails, and asking borrowers to intervene with their employer. Each day without a completed verbal VOE is a day closer to the compliance window closing.

If the window expires, the lender faces a choice: delay closing (risking rate lock expiration and borrower fallout) or close without a compliant verbal VOE (risking buyback on post-closing QC). Neither option is acceptable at scale.

How AI-Agent Outreach Closes the Gap

Superunit's approach to hard-to-reach employers is to initiate simultaneous outreach across phone, email, and fax rather than relying on a single channel. The AI agent handles the call, records the conversation, and generates a transcript with timestamps.

With an average completion time of 0.82 business days, Superunit compresses the outreach timeline from days of manual follow-up to hours. The compliance documentation (call recordings, transcripts, chain of custody) ships with every completed verification, giving QC teams the audit trail that Fannie Mae and Freddie Mac require.

What to Ask Any Verification Provider Before You Sign

Five due-diligence questions that will surface the differences between providers:

- What is your completion rate for small employers not in payroll databases?

- What documentation do you produce for verbal VOE compliance?

- What is your average turnaround time within a 10-business-day window?

- How do you handle employer non-response?

- What is your pricing model if verification is unsuccessful?

The answers to these questions will tell you more about a provider's fit for your pipeline than any product demo. Pay particular attention to the non-response question: every provider succeeds with cooperative employers. Differentiation shows up when the employer doesn't pick up the phone.

Frequently Asked Questions

Does The Work Number satisfy verbal VOE requirements?

No. The Work Number returns historical income and employment records from payroll databases, but Fannie Mae and Freddie Mac require a separate verbal VOE confirming current employment status within 10 business days of the note date. A database lookup does not substitute for that pre-closing contact.

What counts as compliant verbal VOE documentation?

Fannie Mae requires documented evidence of the verbal contact. Freddie Mac's Guide Section 5302.2 requires Form 90 or a similar written record that includes the borrower's name, employer name, and confirmation of current employment. Call recordings, timestamped transcripts, and chain-of-custody records satisfy these requirements and provide a stronger audit trail than a handwritten note.

Can a payroll aggregator like Argyle or Truv complete a verbal VOE?

No. Payroll aggregators pull structured data from borrower-connected payroll accounts. They do not initiate contact with employers, which means they cannot fulfill the pre-closing verbal VOE requirement under Fannie Mae B3-3.1-04 or Freddie Mac Guide Section 5302.2.

What happens if an employer doesn't respond to a verbal VOE request?

The loan file stalls. Without a completed verbal VOE, the lender cannot close within the compliance window without taking on buyback risk. Manual outreach (repeated phone calls, voicemails, borrower intervention) can consume days. If the window expires, the lender must either delay closing or close with an incomplete file.

When should a mortgage lender use Superunit instead of a database solution?

When the borrower's employer is a small business, family-owned company, or any employer not participating in payroll reporting networks like The Work Number. Also when the pre-closing verbal VOE window is tight and manual outreach has already failed or is likely to be slow. Superunit averages 0.82 business days to completion using simultaneous phone, email, and fax outreach.

Matching the Tool to the Use Case

No single verification provider covers every borrower scenario in a mortgage pipeline. Database solutions handle the high-volume, large-employer segment efficiently. Payroll aggregators extend coverage to borrowers on connected payroll platforms. Open banking tools verify income through bank data.

The gap sits with small employers, the 10-day verbal VOE window, and the operational cost of manual outreach. Lenders who build a verification waterfall matching each provider to its strongest use case will close more loans on time, with cleaner compliance files, than those relying on a single vendor to do everything.