A written verification of employment sits at the intersection of two things mortgage operations teams deal with constantly: GSE compliance requirements and employer cooperation. When the employer cooperates quickly, a written VOE is just another document in the file. When they don't, it becomes the single item holding up a closing.

Written VOE differs from verbal VOE in one critical way: the employer must actively complete and return documentation. A verbal VOE allows a lender to call, confirm employment status, and document the conversation. Written VOE requires the employer to fill out a form (typically Fannie Mae Form 1005), sign it, and send it back directly to the lender. The borrower cannot touch the form at any point in that chain.

That dependency on employer action is where the operational risk lives.

When Written VOE Is Required

Written VOE isn't triggered on every loan. Three scenarios commonly require it: variable income that needs employer-level breakdown, part-time employment requiring hours confirmation, and cases where automated data sources don't have the employer on record.

Fannie Mae Requirements

Fannie Mae Form 1005 is the standard written VOE form. The lender completes items 1 through 7, the borrower signs item 8 (the authorization), and the form goes directly to the employer, who returns it directly to the lender. Required fields include employer name, position, date of hire, current salary or pay rate, pay frequency, year-to-date earnings, and likelihood of continued employment.

Per Fannie Mae Selling Guide B3-3.2-01, a written VOE can substitute for paystubs in certain scenarios. Borrowers with variable pay (overtime, bonuses, commissions) where the employer must confirm income breakdown in writing are a common trigger. When paystubs alone don't tell the full income story, underwriters reach for Form 1005.

Freddie Mac Requirements

Freddie Mac Guide Section 5303.1 creates an explicit written VOE trigger: the seller must obtain written documentation from the employer confirming minimum required hours for part-time borrowers. If a borrower works part-time and needs those hours verified, verbal confirmation alone won't satisfy the requirement.

Section 5303.2 provides flexibility on the income documentation side, allowing a paystub, written VOE, or third-party employment verification to each support qualifying income. The practical result is that loan teams choose the path most likely to produce a complete, clean document before the closing deadline.

Lender Overlays

Individual lenders frequently impose stricter written documentation requirements beyond GSE minimums. Some require written VOE for all borrowers regardless of income type, while others mandate it whenever verbal VOE reveals any discrepancy with the application. These overlays mean that even when a GSE guideline technically allows alternatives, your shop's internal policy may not.

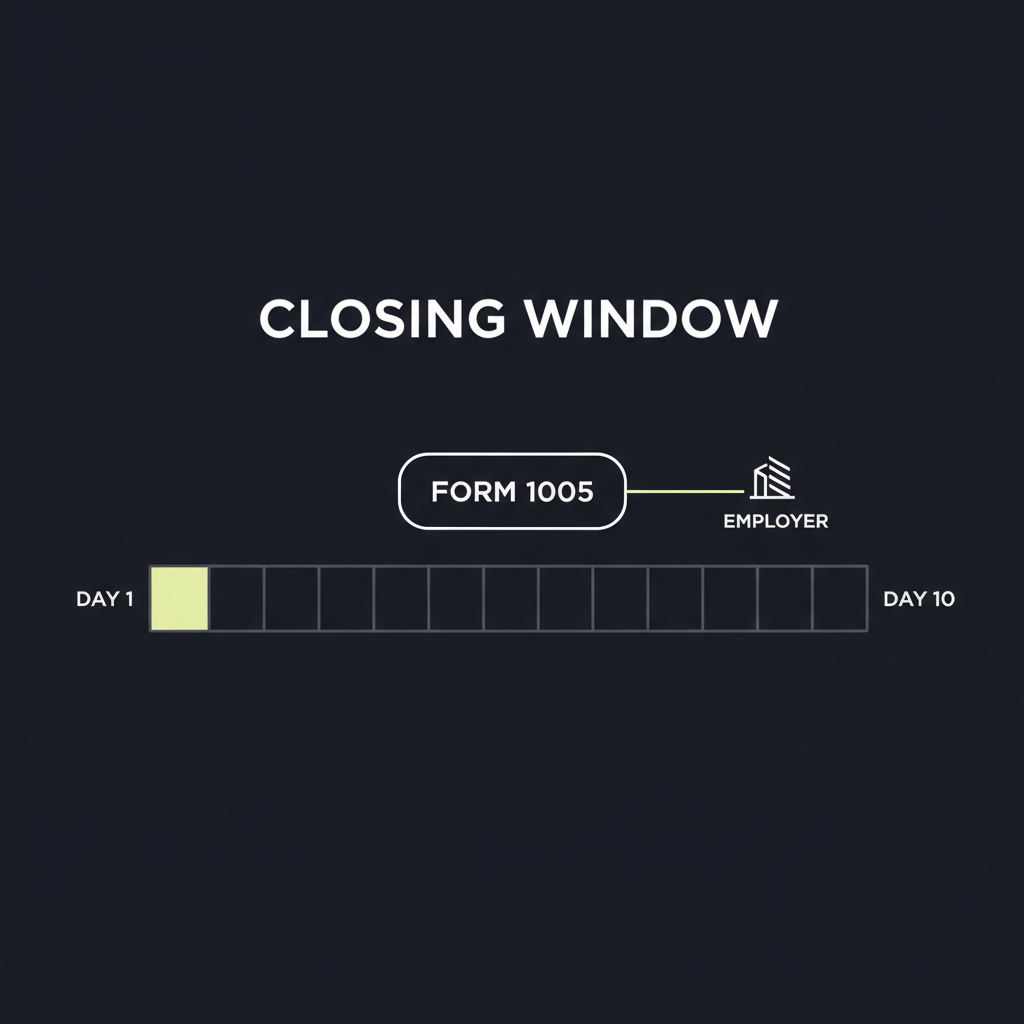

The 10-Business-Day Pre-Closing Window

Both Fannie Mae (B3-3.1-04) and Freddie Mac (5102.4) require employment verification within 10 business days prior to the note date. This window is a hard compliance deadline, not a suggestion. A verification that arrives on day 11 is the same as no verification at all from an audit perspective.

The 10-day window creates compounding pressure when an employer is slow to respond. Manual verification processes can take "from a few days to weeks," while automated or vendor-driven processes can complete verifications "in minutes or hours." When your closing date is fixed and the employer hasn't returned the form, every day of inaction narrows the margin. For a deeper look at managing this timeline, see this breakdown of the pre-closing employment reverification 10-day rule.

The Completion Problem: Why Employers Don't Respond

Written VOE completion rates suffer because the process depends entirely on someone at the employer's office prioritizing a form they didn't ask for. Unlike verbal VOE, where a lender controls the interaction by picking up the phone, written VOE hands control to the employer.

Small Businesses and No-HR Employers

Roughly 33.2 million small businesses in the U.S. employ nearly half the private workforce. In many of those businesses, the owner is the HR department. There's no dedicated team reviewing faxes from mortgage companies, no portal to log into, and no standard procedure for handling a Form 1005.

These hard-to-reach employers represent a disproportionate share of stalled verifications. A restaurant owner juggling a lunch rush is unlikely to treat an unfamiliar fax as urgent. Family businesses, small construction firms, local retail operations, and nonprofits all fall into this category.

The Single-Channel Failure

Sending a single fax or making one phone call to an unresponsive employer is often insufficient. Different employers respond to different channels. Some never check fax machines, some don't answer calls from unknown numbers, and some only engage through email.

A sequential approach (fax first, wait three days, then call, wait again, then email) burns through the 10-day window quickly. Each failed attempt costs time that compounds against the closing deadline.

What Happens When Verification Stalls

A stalled written VOE creates a chain of consequences. The closing date slips, which can push a rate lock past its expiration, exposing the borrower to higher rates or extension fees. In the worst case, the loan is denied entirely if verification cannot be completed within the lender's tolerance window.

For the lender, an incomplete file carries compliance risk during post-close audits. QC reviewers and investors expect to see documentation that matches GSE requirements, and a missing written VOE is a clear deficiency.

How AI-Powered Simultaneous Outreach Solves It

The written VOE completion problem is fundamentally a contact problem. If you can reach the right person at the employer through a channel they actually respond to, the form gets completed. The challenge is figuring out which channel works before time runs out.

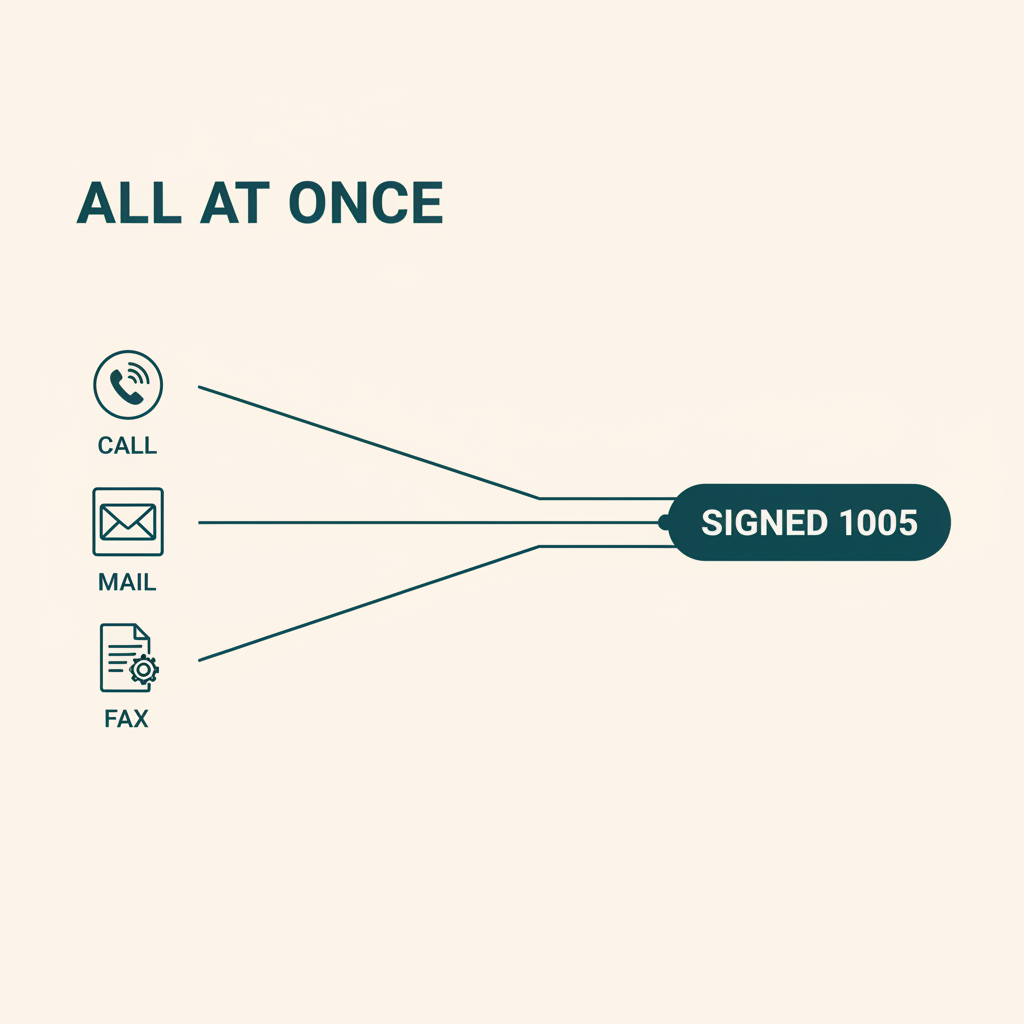

Reaching Employers Across Every Channel at Once

Superunit approaches employer outreach by contacting via phone, email, and fax simultaneously rather than sequentially. Instead of trying one channel, waiting for a response, and escalating to the next, all three channels fire at once. With a database covering approximately 100 million businesses worldwide, Superunit can identify and reach the appropriate contact even when the employer has no formal HR presence.

Parallel outreach solves the single-channel failure described above. If the employer doesn't pick up the phone, they may see the email. If they don't check email, the fax sitting on the machine catches someone's attention during a quiet moment. The probability of at least one channel breaking through is significantly higher than any single attempt.

Speed Inside the Compliance Window

Superunit completes 65% of verifications within 24 hours and 80% within 48 hours. Against a 10-business-day pre-closing window, those turnaround times leave substantial margin for underwriter review and any follow-up questions. The system operates 24/7 without staffing constraints, so outreach doesn't pause for weekends or after-hours gaps.

Compare that to manual processes stretching days to weeks and the difference in pipeline predictability becomes clear. Loan processors spend less time chasing employers and more time moving files forward.

Audit-Ready Documentation by Default

Every interaction Superunit generates is recorded, transcribed, and timestamped. Phone calls produce recordings and transcripts. Email threads are preserved. Fax transmissions are logged with delivery confirmations. All of this creates chain-of-custody documentation that satisfies both underwriter review during origination and investor scrutiny during post-close audits.

For loan ops teams, the documentation value extends beyond a single loan. If an auditor questions the verification process six months later, the timestamped record of every outreach attempt demonstrates good-faith compliance with GSE requirements.

What to Look for in a Written VOE Vendor

Choosing a written VOE vendor is an operational decision with direct impact on closing timelines and audit outcomes. A few evaluation criteria separate vendors that consistently deliver from those that add another layer of uncertainty.

Completion Rate and Turnaround Time

The primary question: can the vendor reliably complete verifications before your closing deadlines? Ask for completion rate data broken out by employer size and industry. A vendor that performs well on large corporations with established HR departments but struggles with small businesses won't solve the hardest part of your pipeline.

Turnaround time distributions (not just averages) are worth requesting. Knowing that 80% of verifications complete within 48 hours tells you more than a vague "average of 2 days" claim.

Multi-Channel Outreach Capability

A vendor that relies on a single outreach method creates the same risk your internal team already faces. Look for simultaneous coverage across phone, email, and fax. Ask whether outreach is parallel or sequential, because the difference directly affects how fast verifications complete within tight compliance windows.

Documentation Quality for Underwriting and Audit

Confirm that the vendor produces records meeting your underwriting standards and capable of surviving post-close QC. Call recordings, transcripts, timestamps, and chain-of-custody documentation should be standard output, not an add-on. Incomplete audit trails create downstream risk that negates the speed benefit.

Pricing Model

Pay-on-success pricing, where the lender pays only for completed verifications, keeps the vendor's incentives aligned with the lender's outcomes. Per-attempt pricing means you're paying for outreach regardless of whether the employer ever responds. Superunit uses a pay-on-success model, which removes the financial risk of unresponsive employers from the lender's side.

One limitation worth noting: Superunit does not cover self-employment verification or scenarios involving defunct employers. Those situations require different documentation paths outside the scope of employer-to-lender written VOE.

Frequently Asked Questions

Is written VOE required for every mortgage?

No. Written VOE is triggered in specific scenarios: variable income requiring employer-confirmed breakdown, part-time employment where minimum hours must be documented (per Freddie Mac 5303.1), and cases where automated data sources don't cover the employer. Many loans are closed with verbal VOE or third-party verification services alone, though lender overlays may impose broader written VOE requirements than GSE guidelines mandate.

Can a borrower provide the written VOE themselves?

No. Fannie Mae Form 1005 must travel directly from the lender to the employer and back. The borrower signs item 8 to authorize the verification, but the completed form cannot pass through the borrower's hands at any point. If an underwriter receives a written VOE that the borrower delivered, the document should be treated as unreliable and a new verification initiated through proper channels.

What if the employer refuses or never responds?

Escalation typically starts with additional outreach attempts across multiple channels. If the employer remains unresponsive, lenders may need to pursue alternative documentation paths such as W-2 transcripts from the IRS, tax returns, or bank statements showing payroll deposits. Some lenders accept a combination of these alternatives in place of written VOE, depending on investor guidelines and the specific income type being documented. Engaging a vendor like Superunit that reaches out simultaneously via phone, email, and fax often resolves the non-response before alternative paths become necessary.