A closing delay caused by a missing verbal verification of employment is one of the most preventable problems in mortgage operations. The requirement itself is straightforward: confirm the borrower is still employed before the loan funds. The execution, especially when an employer won't pick up the phone, is where deals stall.

Both Fannie Mae and Freddie Mac require a pre-closing employment reverification within 10 business days of the note date. The specifics differ slightly between the two agencies, and those differences matter when you're filing documentation or choosing your verification method. Getting the details right protects your closing timeline and keeps the loan saleable on the secondary market.

What the 10-Day Rule Actually Requires

Fannie Mae's Selling Guide (B3-3.1-04) requires lenders to verbally verify a borrower's employment status within 10 business days prior to the note date for any loan that uses employment income to qualify. This verbal VOE for mortgage loans is a non-negotiable step in the closing process. Freddie Mac's Guide (Section 5302.2) imposes the same window but calls it the "10-day PCV" (Pre-Closing Verification), requiring that the verification be obtained no earlier than 10 business days before the note date and no later than the note date itself.

The requirement applies to every conventionally underwritten loan where the borrower qualifies using employment income. It is not reserved for edge cases, risk layering scenarios, or flagged files.

Fannie Mae vs. Freddie Mac: Same Window, Different Forms

Fannie Mae's standard form is Form 1005 (Request for Verification of Employment), though the agency accepts any written record that includes the required data points. Freddie Mac requires Form 90 (Verbal Verification of Employment) or a similar written document.

Both agencies require the same core information in the file: the borrower's current employment status (confirmed as still employed), the name and title of the person who completed the verification, and the date the verification occurred. The practical difference is which form your investor or QC team expects to see in the loan package.

What "10 Business Days" Actually Means

Business days exclude weekends and federal holidays. If your note date is a Monday, the 10-business-day window opened the prior Monday, assuming no holidays fell in between. A Friday note date with a preceding federal holiday means your window is shorter than you might assume if you're counting on your fingers.

The requirement is tied to the note date, not the closing date. In most purchase transactions these are the same day. In delayed funding scenarios, construction loans, or table-funded loans where documents are signed before funding occurs, they can differ. Track the note date specifically.

When Reverification Is Triggered

Every conventional loan using employment income requires a pre-closing VVOE. Whether the borrower is a W-2 employee at a Fortune 500 company or works for a three-person landscaping crew, the requirement applies equally. Processors sometimes treat the VVOE as a formality for "clean" files and a priority only for riskier ones. That distinction does not exist in the selling guides.

The DU Validation Service Exception

As of September 2024, Fannie Mae's SEL-2024-02 announcement introduced an alternative path. Lenders using the DU Validation Service with AccountChek's deposit-based VOE (DVOE) can satisfy the 10-day VVOE requirement without contacting the employer directly, provided the loan closes by the "Close-by Date" generated during underwriting.

There are important limits. The exception applies only to Fannie Mae loans. It does not apply to Freddie Mac loans, which still require the traditional employer-contact PCV. And not all borrowers qualify: the DVOE path requires qualifying payroll deposit patterns in the borrower's bank account data, so borrowers with irregular deposits or multiple income sources may not be eligible.

What Must Be Confirmed and Documented

The minimum data points both agencies require in the loan file:

- Borrower's current employment status (confirmed as actively employed)

- Name and title of the person who completed the verification

- Date the verification was performed

An undocumented verbal contact does not satisfy the requirement. If a processor calls an employer, confirms employment over the phone, and fails to create a written record of that call, the VVOE is incomplete from a compliance standpoint. The written record must be in the file.

Fannie Mae adds one more layer: the lender must independently verify the employer's phone number using a telephone directory, internet search, directory assistance, or licensing bureau. A number provided solely by the borrower is not sufficient on its own.

Acceptable Formats for Completing the VVOE

Both agencies accept multiple verification formats. The choice often depends on what the employer will respond to, not what the processor prefers.

Phone Call

A phone call is the fastest method when the employer answers. The processor calls the employer (at an independently verified number for Fannie Mae loans), confirms the borrower's current employment status, and creates a same-day written log documenting the verifier's name, title, and the date.

The written log is the deliverable, not the call itself. A phone conversation without a corresponding written record in the file leaves the VVOE incomplete.

Written VOE or Work Email Confirmation

A written VOE (Form 1005 for Fannie Mae, Form 90 for Freddie Mac) obtained within the 10-business-day window satisfies the requirement. Alternatively, Fannie Mae accepts an email exchange from the employer's verified work email address, provided the email includes the verifier's name, title, and confirmation of the borrower's employment status.

Personal email addresses (Gmail, Yahoo, Outlook) do not qualify. The email must originate from the employer's domain to be acceptable.

Third-Party Verification Services

Third-party vendors can complete the verbal verification of employment on the lender's behalf. When evaluating mortgage verification providers, consider whether they contact the employer through one or more channels, confirm employment status, and return documentation that meets agency requirements. The DU Validation Service / AccountChek DVOE path described above is one specific version of this, though it works through deposit data rather than employer contact.

Vendor-completed VVOEs are common in high-volume shops where processors manage large pipelines and can't spend hours chasing individual employers by phone.

The Hard-to-Reach Employer Problem

The 10-day VVOE requirement assumes the employer is reachable. In practice, a significant portion of employers are difficult to contact on any given attempt. Small businesses without a dedicated HR department, companies that route all employment verification requests to a single fax number, employers in different time zones, and seasonal operations with inconsistent office hours all create friction.

When the borrower works for a five-person plumbing company and the owner is on a job site all day, a ringing phone with no answer is the most likely outcome of a cold call.

Why Sequential Outreach Fails Under Time Pressure

The typical manual workflow looks like this: processor calls the employer on day one, gets voicemail, leaves a message. Tries again the next business day. Gets voicemail again. By day three or four, the processor has burned a third of the window with nothing to show for it.

Weekends compress the math further. A 10-business-day window contains at most 14 calendar days, and federal holidays can shrink it to 13 or fewer. If you start the VVOE process on day five of the window (which is common when processors are juggling multiple files), you may have three or four actual attempts before the deadline arrives.

What to Do When the Employer Doesn't Respond

Fannie Mae's selling guide does not explicitly address the unresponsive employer scenario. The industry-standard approach involves several steps:

Document every attempt. Record the date, time, phone number called, method used (phone, fax, email), and the outcome of each attempt. Timestamped logs matter for post-closing QC reviews.

Try all available channels simultaneously. If the employer lists a phone number, fax number, and email address, contact all three on the same day rather than working through them one at a time.

Escalate to the borrower. Ask the borrower to alert their employer that a verification call is coming, or to provide an alternative contact (a direct supervisor's line, for instance). The borrower has a vested interest in making this happen.

Consult your underwriter early. If the window is shrinking and the employer remains unresponsive, loop in the underwriter before you're at the deadline. Supplemental documentation like recent pay stubs or W-2s can support the file but are not a substitute for the VVOE itself.

How Simultaneous Multi-Channel Outreach Changes the Math

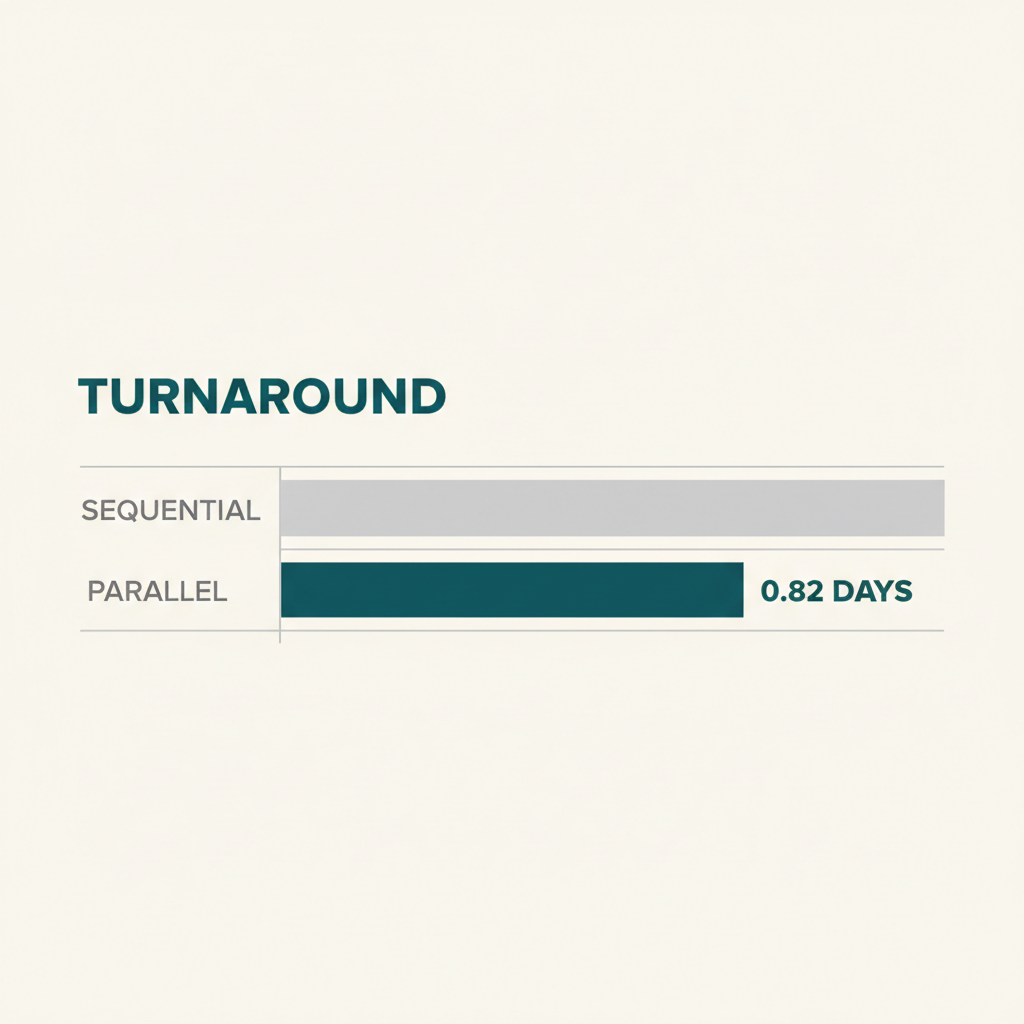

The sequential approach fails because it treats each contact method as a separate step spread across separate days. Reaching an employer by phone, email, and fax on day one, simultaneously, compresses the turnaround dramatically.

Unlike Argyle, Truework, and The Work Number, which rely on payroll database records, Superunit takes a direct-contact approach with AI-driven agents that initiate phone calls, emails, and faxes to the employer at the same time on the first day of outreach. The result is a 0.82 business day average completion time, with 65% of verifications completed within 24 hours. For a processor staring at a closing deadline with an unresponsive employer, that compression is the difference between a smooth close and a delayed one.

Superunit's contact research spans roughly 100 million businesses worldwide, which means the employer phone number can be independently sourced and verified rather than relying on borrower-provided information. That satisfies Fannie Mae's independent verification requirement by default.

The pay-on-success pricing model means processors can initiate the verification without committing budget to attempts that don't result in a completed VVOE. A free tier is available for teams that want to test the workflow before scaling.

Documentation Requirements That Survive an Audit

Post-closing QC reviews and investor audits will look for the VVOE documentation in the loan file. A missing or incomplete record can result in a repurchase demand, a finding on a QC review, or a loan that can't be sold to the intended investor.

What a Compliant VVOE Record Looks Like

At minimum, the file should contain:

- A timestamped record of when the verification occurred

- The name and title of the person at the employer who confirmed the borrower's status

- Explicit confirmation that the borrower was actively employed as of the verification date

- For Fannie Mae loans: evidence that the employer's phone number was independently verified

Whether this lives on a Form 1005, Form 90, a typed call log, or a printed email chain depends on agency requirements and your organization's internal standards. The content matters more than the container, as long as the required form (if any) is present.

How AI-Generated Records Satisfy Documentation Standards

Automated verification services that record and transcribe employer interactions produce documentation that meets and often exceeds what a manual phone log provides. Call recordings capture the exact words spoken. Transcripts provide a searchable, readable record. Timestamped logs create a chain of custody from first outreach attempt through confirmation.

Superunit generates all three automatically for every verification. When an auditor reviews the file six months after closing, the documentation is more detailed than a handwritten note reading "Called employer, spoke with Jane in HR, confirmed employment, 10/15/2024." The recording, transcript, and timestamp log leave no ambiguity about what was confirmed, by whom, and when.

For operations teams managing post-closing QC or responding to investor audits, the difference between "we have a note in the file" and "we have a recording and transcript" is meaningful.

Common Mistakes That Delay or Kill Closings

Four processor errors account for most VVOE-related closing delays. All of them are avoidable.

Starting Too Late in the Window

Processors often initiate the VVOE two or three business days before closing. At that point, a single unresponsive employer can blow the deadline. Starting early in the 10-business-day window gives you room to absorb a few failed contact attempts without jeopardizing the closing date.

If you're using a third-party service like Superunit with sub-one-day average turnaround, the timing pressure eases considerably. But even with fast turnaround, initiating the VVOE as early as the window allows is the safest practice.

Relying on Borrower-Provided Contact Numbers

Fannie Mae requires the lender to independently verify the employer's phone number through a directory, internet search, or licensing bureau. Calling only the number the borrower provided, without independent corroboration, creates a compliance gap that a QC review will flag.

Treating a Voicemail as a Completed Attempt

Leaving a voicemail is a contact attempt, not a completed verification. Employment status must be actually confirmed by a person at the employer. A voicemail left without a return call means the VVOE is still outstanding, and the clock is still ticking.

Missing the Note Date vs. Closing Date Distinction

In most transactions, the note date and closing date are the same. In delayed funding, construction-to-permanent conversions, or scenarios where documents are signed in advance of funding, they can diverge. The 10-business-day window is calculated from the note date. Processors who track only the closing date may find themselves outside the compliant window without realizing it.

The pre-closing verbal VOE is a binary requirement: either the file contains compliant documentation of employment reverification within the 10-business-day window, or it doesn't. No amount of supplemental paperwork fully substitutes for a completed VVOE. The operational challenge isn't understanding the rule. It's executing reliably against it, especially when the employer on the other end of the phone isn't cooperating. Building a workflow that accounts for unresponsive employers from day one, whether through simultaneous multi-channel outreach, early initiation, or automated verification services, is the most reliable way to protect your closing timelines.