TLDR

- Seven platforms compared across six mortgage-critical criteria: coverage depth, turnaround time, LOS integrations, audit trail quality, reverification support, and pricing

- Superunit is the standout for employers outside database and payroll networks, with full audit documentation (call recordings, transcripts, timestamps)

- Database and payroll-connected tools leave a verification gap for smaller employers; Superunit fills it as the third tier in a fallback sequence

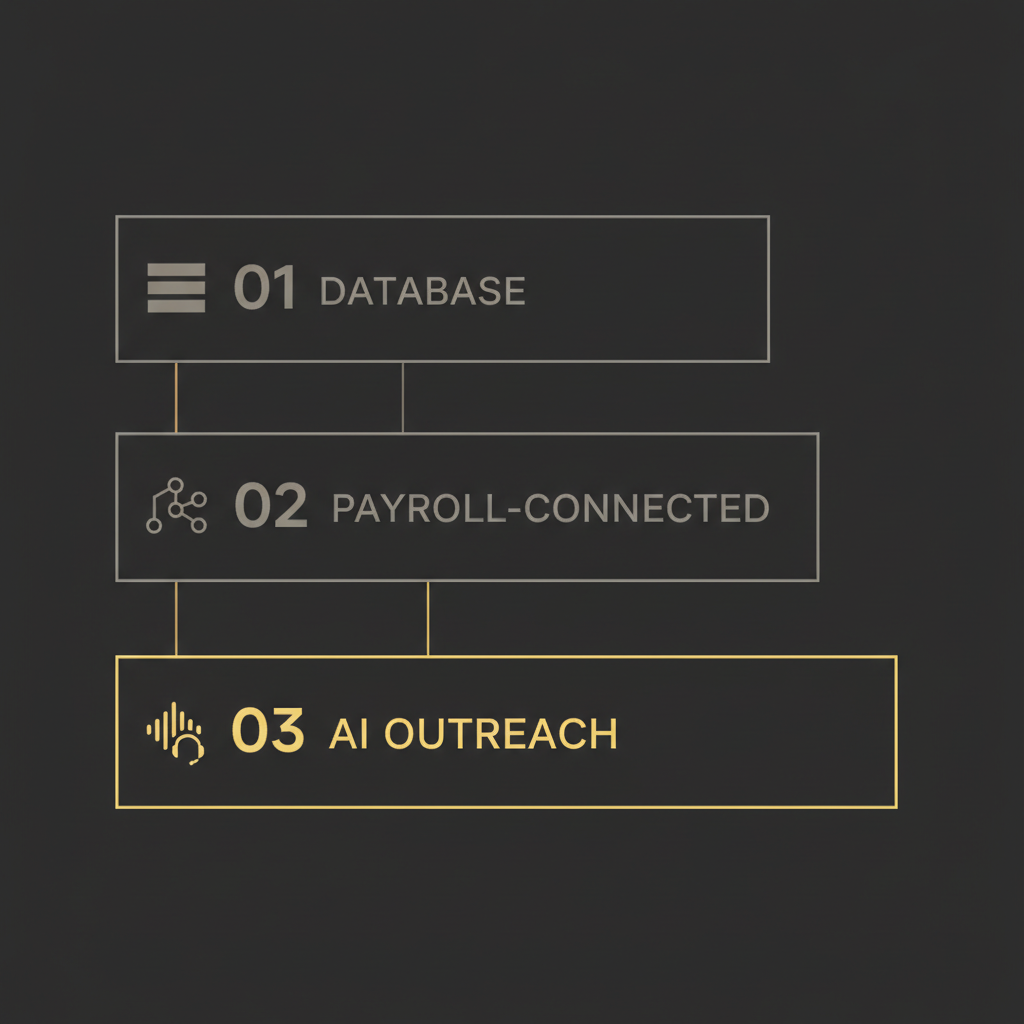

- The 2026 best practice is a tiered approach: database first, payroll-connected second, AI outreach third

- For a deeper breakdown of VOE and VOI options, see our mortgage employment verification providers comparison

A borrower works at a 12-person nonprofit in rural Ohio. The Work Number returns nothing. Argyle can't connect to a payroll provider that doesn't exist in its network. The loan officer picks up the phone, dials HR, gets voicemail, tries again tomorrow, and scribbles a note on the file. Two days pass. The closing deadline is in jeopardy. There's no documented proof of the outreach attempts.

This scenario plays out thousands of times a month across the mortgage industry. Database tools cover large employers well. Payroll-connected platforms handle the next tier. But borrowers at small businesses, nonprofits, and local government agencies fall into a verification gap that costs lenders time, closings, and compliance confidence.

The tradeoff used to be speed versus coverage versus documentation. In 2026, lenders can address all three by stacking the right tools in a tiered sequence. This guide evaluates seven platforms across the criteria that drive underwriting decisions.

What Is Employment Verification for Mortgage Lenders?

VOE (verification of employment) confirms a borrower is currently employed at the stated employer. VOI (verification of income) validates the income figures used for loan qualification, pulling from pay stubs, W-2s, or payroll records. Most loan programs require VOE before approval; VOI requirements vary by loan type and underwriting path. Lenders must also reverify employment before closing, as standard underwriting guidelines for most conventional loans require an employment recheck before final approval.

Three verification models operate in 2026. Database solutions (The Work Number, Experian Verify) pull from employer-contributed records for instant results. Payroll-connected platforms (Argyle, Truv, Truework) access payroll data with borrower permission. AI-driven outreach (Superunit) contacts employers directly when the first two methods return nothing.

The tiered approach is the 2026 best practice: check the database first, try payroll-connected second, then use AI outreach for the rest.

The 7 Best Employment Verification Platforms for Mortgage Lenders

1. Superunit — Best for Non-Database Employers and Compliance Documentation

Best for: Lenders with high volumes of borrowers at small businesses, nonprofits, local government, or any employer absent from database and payroll-connected networks.

Superunit's AI agents contact employers simultaneously via phone, email, and fax. The coverage footprint spans roughly 100 million businesses worldwide, meaning any employer reachable by phone, email, or fax is a candidate. Average completion time sits at 0.82 business days, with 65% of verifications done within 24 hours and 80% within 48 hours.

The compliance angle is where Superunit separates from every other option in this comparison. Every call is recorded, transcribed, and timestamped, producing a chain-of-custody record that goes well beyond a standard database confirmation. For compliance managers running QC audits, hearing the actual recorded conversation with an employer's HR department at 2:14 PM on Tuesday carries more weight than a static data pull receipt.

Pay-on-success pricing means lenders pay nothing for failed verification attempts.

Pros:

- 0.82 business day average turnaround, with 80% of verifications complete within 48 hours

- Call recordings and transcripts for every employer interaction provide the strongest audit trail in this comparison

- Covers employers outside database networks including small businesses, nonprofits, and local government that TWN and Experian Verify miss entirely

- Pay-on-success pricing eliminates wasted spend on verifications that don't complete

- AI agents run unlimited simultaneous outreach attempts, scaling instantly without adding headcount

- Up to 80% cost reduction versus manual screening processes

Cons:

- No instant results for large-employer borrowers; Superunit is not a database solution and should sit behind TWN or Experian Verify in a tiered sequence

- API-only integration with no native Encompass embed yet, which adds implementation work for teams on that LOS

- Newer company (2024) with less brand recognition in mortgage than established players like Equifax or Truework

Pricing: Pay-on-success with a small flat fee per successful verification. Free tier available. Custom enterprise pricing on request.

2. Truework — Best Multi-Method Cascade for Encompass Users

Best for: Lenders on Encompass or Blend who want a single vendor managing database, payroll-connected, and manual verification in one workflow.

Truework claims 75% coverage through its built-in cascade, which tries database records first, then payroll connections, then manual outreach. Truework Intelligence, launched in March 2025, adds predictive modeling to route verifications more efficiently. Confirmed integrations with Encompass and Blend, plus a TransUnion partnership announced in March 2025, expand Truework's data access for mortgage lenders.

Pros:

- Encompass and Blend integrations confirmed, fitting the two most common mortgage origination platforms

- TransUnion partnership (March 2025) expands VOIE data access beyond Truework's own database

- Transparent pricing at $59.95 (VOE), $64.95 (VOI), and $19.95 (reverification VOE)

- Built-in cascade reduces vendor management overhead for ops teams

Cons:

- Manual fallback process lacks detailed documentation such as call recordings or interaction transcripts, which limits QC audit depth

- 75% coverage claim still leaves one in four verifications potentially unresolved within the platform

Pricing: VOE $59.95 / VOI $64.95 / Reverification VOE $19.95.

3. Argyle — Best LOS Integration Footprint for Payroll-Connected Verification

Best for: Lenders on Encompass, Vesta, BytePro, or LenderLogix who want real-time payroll-connected VOI, VOE, and VOA from a single platform.

Argyle reported 192% mortgage growth in its 2025 mid-year review and has the broadest LOS integration footprint of any payroll-connected provider. The upgraded Encompass integration and Consumer Connect both launched in May 2025. Vesta LOS integration followed in March 2026, with LenderLogix added in August 2025. Argyle is eligible for Fannie Mae rep and warrant relief, which reduces repurchase risk for compliant loans.

Pros:

- Broadest LOS footprint among payroll-connected providers (Encompass, Vesta, BytePro, LenderLogix)

- Real-time payroll data delivers VOI, VOE, and VOA results in minutes

- Fannie Mae validation solutions eligible for rep and warrant relief

- 192% mortgage growth in 2025 signals strong market traction and lender adoption

Cons:

- Borrower authentication required to connect payroll accounts, which introduces friction and can stall some borrowers

- Coverage depends on payroll platform availability, so employers on unsupported or legacy systems return no results

- Pricing not publicly listed, requiring a sales conversation to evaluate cost

Pricing: Contact sales.

4. The Work Number (Equifax) — Best Database Coverage for Large-Employer Borrowers

Best for: Lenders whose borrower base is concentrated at Fortune 500 companies, government agencies, and employers using major payroll processors.

The Work Number holds the largest employment database in the US, returning instant results in seconds for covered employers. It sits within Equifax's TotalVerify hub and supports both Fannie Mae validation solutions and Freddie Mac AIM for rep and warrant relief. The Report Indicator feature, launched in March 2025, flags upfront whether a borrower has a VOIE record in the database before the lender orders (and pays for) a full verification.

Pros:

- Largest US employment database with instant results for hundreds of millions of records

- GSE-approved for Fannie Mae rep and warrant relief and Freddie Mac AIM

- Report Indicator (March 2025) prevents wasted spend by flagging record availability before ordering

- Reverify Now allows online employment reconfirmation before closing

Cons:

- Small businesses, nonprofits, gig workers, and self-employed borrowers are absent from the database entirely

- Premium pricing without publicly listed rates makes cost comparison difficult

- No built-in fallback mechanism when a borrower's employer isn't in the database, leaving lenders to source a separate solution

Pricing: Contact sales. Per-verification rates vary by time frame and purpose.

5. Truv — Best Pay-Per-Success Payroll-Connected Option

Best for: Cost-conscious lenders who want GSE-approved payroll-connected verification without subscription commitments or setup fees.

Truv operates a consumer-permissioned payroll data platform with direct-to-source payroll, bank data, and document upload capabilities. The pay-per-success model charges nothing for unsuccessful attempts and requires no setup fees or long-term contracts. Truv is Freddie Mac approved and Fannie Mae DU eligible, and it's available through SettlementOne's multi-vendor cascade.

Pros:

- Pay-per-success, no setup fees and no long-term contracts lower adoption risk

- GSE-approved for Fannie Mae DU and Freddie Mac AIM

- Available via SettlementOne cascade alongside TWN and Experian Verify for broader coverage

- Transparent pricing published at truv.com, claiming up to 80% cost savings versus traditional verification

Cons:

- Smaller LOS integration footprint than Argyle or Truework, with nCino as the primary confirmed integration

- Borrower authentication required, adding friction to the verification process

- Coverage ceiling matches other payroll-connected tools, limited to employers on supported payroll platforms

Pricing: Pay-per-success with transparent rates at truv.com. No setup fees or long-term contracts.

6. SettlementOne — Best Single-Vendor Relationship for Multi-Source Cascade

Best for: Lenders who want one vendor relationship managing a multi-source verification cascade without building custom integrations to each provider.

SettlementOne is a mortgage services aggregator, not a verification technology company. It resells access to The Work Number, Experian Verify, Truv, and manual verifications through its VOE/I Cascade product. Encompass Partner Connect integration is confirmed.

Pros:

- Access to TWN, Experian Verify, and Truv through a single platform and vendor relationship

- Cascade automation routes verifications through available sources without manual decision-making

- Encompass Partner Connect integration confirmed for the dominant mortgage LOS

Cons:

- No proprietary coverage advantage since SettlementOne resells others' data and technology

- Manual fallback uses traditional phone and fax outreach without recorded interactions, limiting audit trail depth

- Aggregator markup on underlying vendor rates reduces pricing transparency

Pricing: Contact sales. Rates vary by underlying vendor.

7. Experian Verify — Best for Lenders Already in the Experian Ecosystem

Best for: Lenders already using Experian for mortgage credit reports who want to consolidate verification under the same vendor relationship.

Experian Verify is a database-driven VOIE product with millions of payroll records and GSE approval for Fannie Mae and Freddie Mac validation solutions. The Preview Report, launched in April 2026, gives lenders upfront visibility into whether an employer record exists before ordering a full verification, at no cost to existing Experian mortgage clients. Experian Verify is available through SettlementOne's cascade and Xactus partnerships.

Pros:

- GSE-approved for Fannie Mae and Freddie Mac validation solutions

- Preview Report (April 2026) eliminates wasted pulls by showing employer availability upfront, free for existing clients

- Existing Experian relationships via credit reporting make vendor onboarding straightforward

Cons:

- Same database coverage limits as The Work Number: small employers, nonprofits, and gig workers are absent

- Pricing not publicly listed, making cost evaluation opaque

- Fewer confirmed LOS integrations than Argyle or Truework

Pricing: Contact sales. Preview Report free for existing Experian mortgage clients.

Summary Comparison Table

| Platform | Model | Turnaround | LOS Integration | Audit Trail | Reverification | Pricing |

|---|---|---|---|---|---|---|

| Superunit | AI outreach | 0.82 business days avg | API | Call recordings + transcripts + timestamps | ✓ | Pay-on-success |

| Truework | Cascade (DB + payroll + manual) | ~24 hours | Encompass, Blend | Digital records | $19.95 VOE | $59.95 VOE / $64.95 VOI |

| Argyle | Payroll-connected | Real-time | Encompass, Vesta, BytePro, LenderLogix | Payroll data trail | Yes (refresh in LOS) | Contact sales |

| The Work Number | Database | Instant | TotalVerify hub | Database pull record | Reverify Now | Contact sales |

| Truv | Payroll-connected | Instant | nCino, SettlementOne | Payroll data trail | ✓ | Pay-per-success |

| SettlementOne | Aggregator (TWN + Experian + Truv) | Varies | Encompass Partner Connect | Varies by vendor | Yes (via underlying vendors) | Contact sales |

| Experian Verify | Database | Instant | SettlementOne, Xactus | Database pull record | ✓ | Contact sales |

For a deeper comparison of Argyle, Truework, The Work Number, and Superunit, see our side-by-side breakdown.

Ready to close the verification gap for small-employer borrowers? Start free today

Why Superunit Is the Right Choice for Employers Outside Database and Payroll Networks

Database and payroll-connected tools cover large employers and digitally connected payroll providers effectively. They leave borrowers at smaller organizations unverified: the small businesses, nonprofits, local government offices, and other employers that don't contribute records to databases or use compatible payroll systems.

Superunit's AI agents fill that gap with documented, timestamped outreach rather than undocumented manual phone calls. Average turnaround is 0.82 business days. That matches or beats manual fallback timelines at a fraction of the cost. Recorded employer conversations with full transcripts give compliance and QC teams verifiable evidence of each interaction, not just a confirmation that a record existed in a database at a point in time.

Pay-on-success pricing eliminates wasted spend. Superunit is best positioned as the third tier in a verification sequence: The Work Number or Experian Verify first, Argyle or Truv second, Superunit for the employers those tools cannot reach.

How We Chose the Best Employment Verification Platforms for Mortgage Lenders

We evaluated six criteria: coverage depth, turnaround time, LOS integrations, audit trail quality, reverification support, and pricing transparency. LOS integration weighting favored Encompass compatibility since it remains the dominant mortgage loan origination system.

Audit trail quality was assessed by documentation type. A database pull record confirms a data point existed at a moment in time. A recorded, transcribed employer conversation with a precise timestamp documents what was said, by whom, and when, which is a meaningful distinction for compliance teams and QC auditors.

GSE compliance pathways (Fannie Mae rep and warrant relief, Freddie Mac AIM) factored into database and payroll-connected rankings. We reviewed 2025 and 2026 product announcements for each vendor, assessed pricing transparency (published rates versus contact-sales-only), and evaluated coverage of non-database employers as a standalone criterion.

FAQs

What is VOE and VOI in mortgage lending?

VOE confirms a borrower is currently employed at the stated employer. VOI validates the income figures used for loan qualification, drawing from pay stubs, W-2s, or payroll records. Superunit handles both through AI-driven employer outreach, with every interaction recorded, transcribed, and timestamped. For a full breakdown, see our VOE/VOI mortgage guide.

Do mortgage lenders have to reverify employment before closing?

Standard underwriting guidelines for most conventional loans require an employment recheck before final approval. Most platforms support reverification; Truework charges $19.95 per VOE reverification. Superunit re-contacts the employer via AI agents and documents the interaction with a recorded, timestamped confirmation.

What happens when a borrower's employer isn't in The Work Number database?

The Work Number returns no result, and the lender must use a fallback vendor. Payroll-connected tools like Argyle and Truv require borrower authentication and may also fail if the employer isn't on a supported payroll platform. Superunit contacts the employer directly via phone, email, or fax, requiring no database record or payroll connection.

Is Superunit better than Truework for mortgage verification?

They serve different roles. Truework covers a broader range of borrowers through its built-in cascade (database, payroll-connected, manual). Superunit is built for the employers that Truework's cascade cannot reach. Where Superunit clearly leads is documentation depth: every employer interaction is recorded with a full transcript, while Truework's audit trail draws from digital records generated by database and payroll sources.

What LOS integrations should I prioritize when evaluating verification platforms?

Encompass by ICE Mortgage Technology is the dominant mortgage LOS, so confirmed Encompass integration should be a baseline requirement. Argyle has the broadest payroll-connected LOS footprint (Encompass, Vesta, BytePro, LenderLogix). Superunit currently integrates via API without a native Encompass embed, which is a known limitation.

How does the tiered approach work in 2026?

Step 1: Check database availability using The Work Number Report Indicator or Experian Verify Preview Report before ordering a full verification. Step 2: If no database record exists, try payroll-connected verification through Argyle, Truv, or Truework. Step 3: If payroll-connected verification fails, use AI-driven outreach through Superunit for employers outside those networks.

What is the best alternative to The Work Number for small-employer borrowers?

The Work Number has no coverage for small businesses, nonprofits, or gig workers. Payroll-connected tools (Argyle, Truv) require borrower authentication and may also miss small employers on unsupported payroll systems. Superunit contacts the employer directly, making it one of the few scalable options for non-database, non-payroll-connected employers.

How quickly can Superunit complete a verification?

Superunit averages 0.82 business days per completed verification. 65% finish within 24 hours, and 80% finish within 48 hours. That's 3 to 5 times faster than traditional manual screening, with the added benefit of full documentation for every outreach attempt.

Close the verification gap for borrowers at smaller organizations. Start free today